Berkeley Group Holdings recently fell around 15% after a few hedge funds shorted the London housing market in the midst of panic. The funds believe there are pockets of oversupply in London and pressure from emerging market demand that will cause a supply-demand imbalance. The FT also recently released news that the price per square foot for prime London property dropped from £1,839 to £1,813 last year, indicating signs of a reverse of the excess demand in the market we have seen.

Are these macro funds playing on recent macroeconomic developments such as the effects of falling oil prices on emerging, most probably Russian and Chinese, demand for London property and FX devaluations? These short sellers led me to check some numbers to test the potential damage to Berkeley.

The two driving factors in any homebuilders’ margins are the cost of land and final sales price.

Figure 1 shows the average selling price was £575k in 2015, up from £280k in 2012. This is huge and unsustainable growth in prices. BKG also mention 2015 average selling price was driven by sales mix at the very top end of the market.

Land costs as a percentage of final selling price peaked in 2014 at 17.3% and is 15.2% on average over the last 5 years.

Figure 2 shows the upward trend of land cost in absolute values. The average value of land between 2012-15 was £66,000. This is nearly double the average over the previous 8 years. This is mainly because in 2013 and 2014 they purchased 5,500 plots of land in London for on average £121,000. These were all in prime spots, Canary Wharf, Dockland’s Wimbledon etc. I believe these are the purchases the hedge funds believe are bought near the top of the cycle and, therefore, will depress earnings. However, this represents only a small portion of the land held by BKG.

Figure 3 above shows the growth in plots in BKG land bank which can be misleading. The huge jump of around 10,000 plots in 2015 is due to the long-term options they purchase through time finally being approved for development. These are plots of land that are bought years earlier, at cheap brownfield prices, and are now ready to begin development. This is where BKG earn their superior margins.

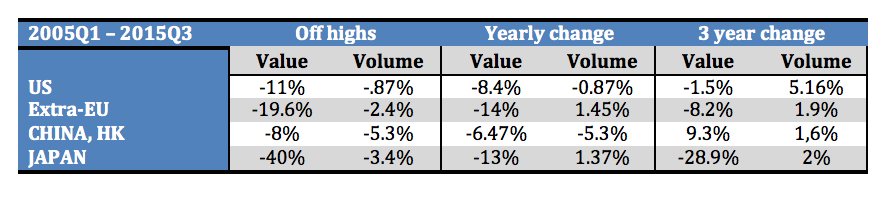

So how much damage can the £600m purchase of land at, potentially, the top of the cycle do to future earnings? We don’t get the margins for individual projects although we can make some rough estimates. Figure 4 below shows the average price for new dwellings fell max 15% and 9% in London and the South East respectively during the financial crisis.

Rightmove show the average current prices of Greater London to be around £610,000 and at the top end, which Berkeley certainly will be supplying with the £600m of acquisitions, £1.5m.

If we assume one plot is minimum one home. This means the most recent acquisitions of £121,000 per plot in Greater London were the land cost for each home. At a 33% discount to the average price in London, the selling price would be £400,000 for these plots. This gives them plenty of room to not actually destroy value with this purchase even in worse case scenario.

Can these external macro factors really disrupt Berkeley’s fundamentals?

Demand

BKG look to sell houses forward to reduce risk. They currently have around £3bn of forward sales due in the next 3 years under UNCONDITIONAL contracts. These forward sales increased by £685m from 2014 to 2015, an increase of 30.1%. Forward sales have a CAGR of 29% over the last 5 years. Customers are increasingly buying homes from Berkeley before they are even built. Berkeley currently holds £920m from deposits on these forward sales, around 30% deposit rate.

Berkeley’s customers include housing associations, providers of student accommodation, investors and first-time buyers. In 2014 BKG opened international offices in Dubai and Beijing because over the five years to 2014 £1.2bn in sales had come from overseas. After all, BKG have got properties available in London for up to £23m!!

The Residential Institute for Chartered Surveyors residential market survey provides a good indicator of the industry supply and demand balances. The February 2016 release concludes:

- London has seen an uptick in new sales listings in the last few months.

- New buyer enquiries rose for 10-month. Demand is being bolstered by buy-to –let investors before the 3% surcharge policy in April.

- 50% of surveyors also believe this charge will cause a slowdown in investment after the surcharge.

- Excess demand oversupply persists, prices remain firmly in up-trend. 72% more surveyors believe prices will continue this trend.

- 65% of surveyors believe London and South East is above fair value to some extent. However, this number has not changed in 6 months.

- South East region is increasingly under-supplied.

This survey provides great insight into real industry trends and developments. The April 3% Stamp Duty surcharge for buy-to-let will cause rapid demand in Q1 which will likely fall thereafter. Prices will lag and, therefore, I believe that towards the end of 2016 we could see a larger slowdown in prices in London (which will then encourage first-time buyers who seem to be waiting).

This survey provides great insight into real industry trends and developments. The April 3% Stamp Duty surcharge for buy-to-let will cause rapid demand in Q1 which will likely fall thereafter. Prices will lag and, therefore, I believe that towards the end of 2016 we could see a larger slowdown in prices in London (which will then encourage first-time buyers who seem to be waiting).

It’s clear that Britain needs more homes to meet rising demographics and population growth in the long term. In 2010, and later extended in 2014, the government set a target to build 1m homes on brownfield sites by 2020 in total. There is plenty of support from the government helping Berkeley build the houses on brownfield land although they are still well below target building only 176,000 total in 2015. The ONS also estimate there is around 2800 and 6000 hectares of brownfield land available for dwellings in London and the South East respectively.

On the whole, I feel the macro funds are making a bold bet against the fundamentals of the housing market. Also, I think there is a slight chance this was a very short-term trade from the hedge funds to take advantage of short-term panic. There are definitely pockets of fair-overvalued properties in London and even recent scares of oversupply. However, I feel there is still a huge fundamental imbalance of demand and supply that persists and, unless there is a recession precipitated by some kind of China hard-landing, Berkeley should be somewhat protected. I will be keeping a close eye on the RICS report in 2016.

Valuation

Simply discounting the £2 dividends you’re almost certain to receive annually at a cap range of 8-10% gives around £5 NPV today. Last year EPS was £3.13, assuming this does not grow in 3 years and using a multiple of 10 gives £35 as a back of the envelope value.

Book value is £1.76bn and priced at 2.4x. Very pricey relative to comparables, although not when you consider the assets booked at cost. BKG has 38,000 plots of land booked as cost on their balance sheet. This equates to £5.15bn in future gross margin at an average selling price of £456,000. At a price of £400,000 this equates to £4.56bn, roughly their market cap today. I will take the option that the average selling price will be above £400,000 and Berkeley management will continue to be purchase cheap brownfield land in the future.